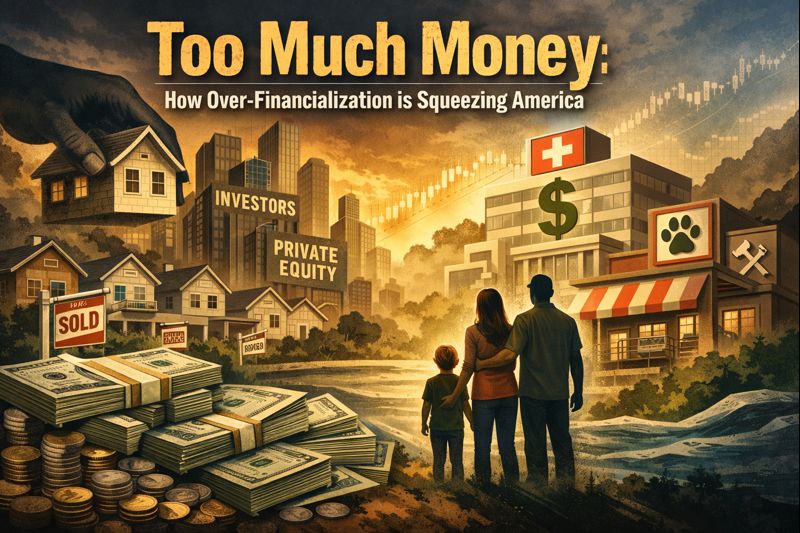

In an era where capital seems endless, the real problem isn’t scarcity—it’s excess. Too much money sloshing around in the system has turned everyday essentials like housing, healthcare, and local services into playgrounds for investors and private equity firms. This flood of cash, fueled by low interest rates, quantitative easing, and tax incentives, has driven up prices, degraded quality, and locked out ordinary folks. But there’s a silver lining on the horizon, particularly in housing, as demographic shifts promise to shake things up. Let’s dive into the data and see why it’s time to get the big money out.

The Housing Bubble: Not a Supply Shortage, But an Investor Feast

We’ve all heard the mantra: “Build more houses!” But the data tells a different story. The issue isn’t an absolute lack of homes; it’s who owns them and why. Baby Boomers, born between 1946 and 1964, currently hold about one-third of all U.S. homes, amounting to a staggering $19.7 trillion in real estate value. As this generation ages, their properties are set to flood the market through sales, downsizing, or inheritance.

Projections from sources like Fannie Mae and the Mortgage Bankers Association paint a clear picture: Between 2016 and 2026, older homeowner exits are expected to release 10.5 to 11.9 million units. That number jumps to 13.1 to 14.6 million from 2026 to 2036—a 42% increase. This could add around 250,000 excess units annually, based on demographic trends alone. Dubbed the “Silver Tsunami,” this wave is anticipated to ease supply constraints in many markets, potentially cooling prices.

Yet, this natural rebalancing is threatened by investors hoovering up inventory. Investors—both individual and institutional—own 18-20% of the nation’s 86 million single-family homes. In Q3 2025, they snapped up 34% of all home purchases, the highest share in five years. While large institutions hold just 0.35-3% nationally (with higher concentrations in places like Atlanta at 10% of rentals), small investors dominate, controlling 85-90% of investor-owned properties.

What fuels this frenzy? Tax perks like depreciation. Owners of rental properties can deduct the building’s cost over 27.5 years, shielding income from taxes even as values rise. For a $825,000 building, that’s about $30,000 annually in deductions. Add bonus depreciation for improvements and 1031 exchanges to defer gains, and you’ve got a system rigged for endless accumulation. Eliminating these on second, third, or more homes could deter hoarding and free up stock for families.

Deregulation isn’t the answer—it would just invite more builds for investors to gobble. We need policies that prioritize owner-occupants, like caps on multiple-home ownership or revamped taxes, to let the Boomer exodus truly reset the market.

Private Equity’s Tentacles: Corporatizing Everything from Vets to Roofers

The “too much money” problem extends far beyond housing. Private equity (PE) firms, armed with trillions in dry powder—$5.8 trillion globally as of 2026—are rolling up industries through “buy-and-build” strategies. They acquire small businesses, consolidate them, load on debt, and squeeze for profits, often at the expense of quality and affordability.

In healthcare, PE has invested $1 trillion over the past decade, including $200 billion in 2021 alone. Veterinary care saw a 659% surge in PE/VC funding to $2.89 billion in 2023, with consolidators now owning about 50% of clinics. Roofing companies, A/C contractors, and other home services are prime targets for similar roll-ups, part of over $100 billion in M&A activity.

The fallout? Higher prices, standardized (often subpar) services, and worker burnout. In vets, it’s pricier care with a profit-first mentality; in healthcare, reduced access and quality dips. Even chains like Subway or Jersey Mike’s, post-buyout, resort to shrinkflation—smaller portions for the same price.

While PE touts efficiency and growth, the reality is over-financialization: Too much capital chasing yields, turning local economies into extraction machines. Scrutiny is rising—states are eyeing laws to curb PE in healthcare, and deal volumes are set to climb in 2026 despite risks.

Time to Drain the Swamp

The common thread? Excess liquidity from years of easy money policies has inflated asset bubbles and enabled PE’s sprawl. In housing, the Boomer die-off offers a natural correction, but only if we boot investors via tax reforms. Across sectors, kicking out corporatization could restore competition, lower costs, and revive community-driven businesses. It’s about less regulation—it’s about smarter rules that favor people over profits.

With $5.8 trillion in PE dry powder waiting to deploy, the pressure won’t ease without action. Let’s make “too much money” a problem of the past.

What do you think, Nostr?